Abnormal Sample

of Liaoning Province should not be calculated into the Evaluating on the

Continuous Falling Investment

Moreover, the

continuous fallback of the investment on the fixed asset varied with the

present policies of stabilizing growth. According to statistics, the investment

on the fixed asset obviously fell back in July, the year-on-year growth, which

turned to be the lowest level since 1999, declined from 9% to 8.1%. However,

according to investigation, currently, the data of fixed asset investment is

actually, or we can say to a great extent, distorted by the huge abnormal

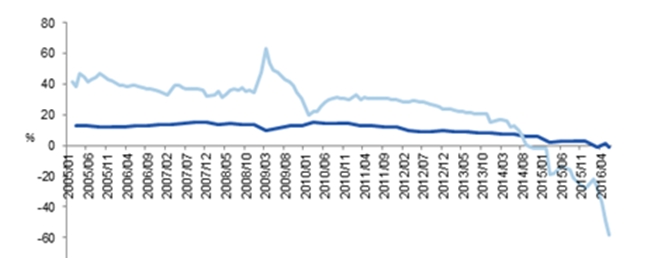

reduction of Liaoning Province. For example, during H1 2016, total fixed-asset

investment declined by 58.1% YoY in Liaoning, whose growth rate of fixed-asset

investment had once been 60% since financial crisis and then plummeted since

2015. The reasons for this phenomenon on the one hand were the economic decline

and on the other hand related to the accuracy of statistical data. For example,

before 2006, the formation of the fixed-asset in Liaoning highly coincided with

the proportion of the fixed-asset investment to GDP, but during 2008 to 2014,

the difference between the two data gradually enlarged, and not until the year

after 2014, the gap between those two set of data narrowed. The abnormal

fluctuations of fixed-asset investment data disturbed analyzing on the actual

situation of investment.

Graph 4:

Investment on Fixed-Asset Plummeted in Liaoning Province since 2015

GDP of Liaoning Province Fixed-asset investment of Liaoning Province

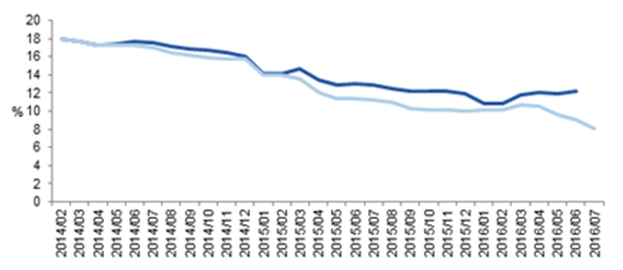

However, the

growth of fixed-asset investment in other provinces rebounded backed by the

fiscal incentive of local governments this year. From the overall situation,

the abnormal data of Liaoning Province disturbed the overall trend of other

provinces, while after taking the data of Liaoning out, China’s domestic

fixed-asset investment can be relatively kept in a stabilized situation, from

this perspective of view, under the influence of the measure of stabilizing

growth, the present fixed-asset investment data tended to be stabilized.

Graph 5:

Relatively Stabilized Fixed-Asset Investment across the Nation (Except

Liaoning)

Fixed-Asset Investment except Liaoning Province Fixed-Asset Investment

Sluggish Credit and Loan Data should take the

Influence of Debt Replacement into Consideration

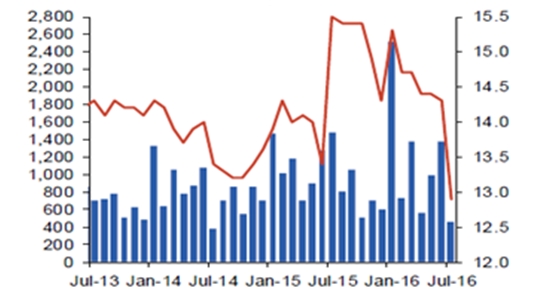

The credit and

loan data of July was also noteworthy. RMB loan increased by RMB463.6 billion,

RMB1.01 trillion less than that of the same period last year, among which the

loan of non-financial enterprises and group decreased by RMB2.6 billion, while

the loan of department increased by RMB457.5 billion. According to this data,

currently the real economy has hardly had any need in credit and loan, which

indicated a sign of sluggish economic activity. However, interpreting credit

and loan data should also take the influence of the debt replacement of the

government into consideration. In 2016, the debt replacement of the government

exceeded RMB5 trillion, which was RMB4,000 to 5,000 trillion in average each

month. The situation of credit and loan may not as negative as what the

negative growth has showed in July if we take the debt replacement of local

government into consideration.

Graph 6: Newly-Added Debt in July Neglected the Influence from Debt Replacement

Newly-Added Debt (billion) Year-on-Year Change (right axis)

Therefore, it is

believed that it’s necessary to integrate various data to analysis the current

economic data of China. For example, the data of industrial added value,

electric power output, and industrial enterprises profits were in directional

deviation when considering the actual situation of industrial production. And

according to the statistics, among the current industrial economic operation,

the positive factors have kept building up, the accumulation of new energy has

accelerated, and the high-end industry segments still in high speed increase,

therefore we can see that the actual industrial production was not as negative

as the continuously decreasing industrial added value. In the same way, the

data of the current investment and the credit and loan may be slightly positive

than the actual data if the abnormal data of Liaoning was eliminated and the

debt replacement factor was taken into consideration.

However, the risks

were also noteworthy. On the one hand, the economic structural problems

remained serious, the price of the real estate in major cities keep rising,

which formed a crowding-out effect on the real economy, moreover, under the

background of the Federal Reserve of the US raising the interest rate, boosted

the pressure on capital outflow and depreciation of exchange rate.

On the other hand,

the policy space is reducing. The year-on-year growth of the fiscal general

expenditure plummeted from 20% of June to 0.3% of July, growth of M2 decreased

from 11.8% of June to 10.2% of July, and the newly added RMB debt decreased by 68.7%

YoY, these three factors all together were important reasons for the declining

economic data.

In terms of the

monetary policy, in China, there are risks from the real estate market and

financial market, while overseas, with the expectation that the Federal Reserve

raising the interest rate, RMB depreciating, and the capital outflow and the

reality that the monetary policy was not as easy as that of the first half

year, the central bank would not reduce the interest rate and deposit reserve

ratio. In terms of fiscal policy, as there has already faced deficit during the

first half year, the space of the second half year would be limited, which we

can forebode from the 0.3% of the year-on-year growth in general fiscal

expenditure and 7.4% YoY decrease of expenditures incurred directly by the

central government in July.

*The

article is edited and translated by CCM. The original one comes from Laohucaijing.com.

About CCM:

CCM is the leading market intelligence

provider for China’s agriculture, chemicals, food & ingredients and life

science markets. Founded in 2001, CCM offers a range of data and content solutions, from price

and trade data to industry newsletters and customized market research reports. Our clients include Monsanto, DuPont, Shell, Bayer, and Syngenta. CCM is a

brand of Kcomber Inc.

For

more information about CCM, please visit www.cnchemicals.com or

get in touch with us directly by emailing econtact@cnchemicals.com or

calling +86-20-37616606.